Advice from the Experts

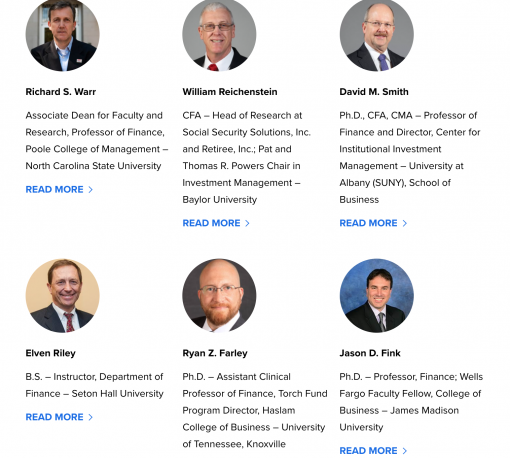

Richard S. Warr

Associate Dean for Faculty and Research, Professor of Finance, Poole College of Management – North Carolina State University

“My advice to my students and to anyone who will listen is to always take the long view. Many people panicked and sold in March last year after the market crashed only to find themselves having to buy back into a rapidly rising market. So the best strategy for an individual investor is to stay the course and maintain a very well-diversified portfolio. But I do think that the gyrations back in the spring of 2020 provide investors with an example of what can happen in a crisis. The market dropped nearly 30% in a couple of weeks. Investors should ask themselves – am I comfortable with a 30% drop that might take a long time to recover from? If they are uncomfortable with this level of volatility, then I would suggest re-weighting their portfolios to be a little less risky by increasing their holdings in bonds.”

William Reichenstein

CFA – Head of Research at Social Security Solutions, Inc. and Retiree, Inc.; Pat and Thomas R. Powers Chair in Investment Management – Baylor University

“For a perspective on international stock allocation for retirees within a well-diversified portfolio, I turn to Vanguard, Fidelity, and T Rowe Price. Diversification means not putting almost all your “eggs” in the same basket, even if that basket is the USA. The Vanguard Target Retirement Income Fund (VTINX) is intended for people 72 and over. Its target asset allocation is 30% stocks, including 40% of this stock allocation (thus 12% of total allocation) in international stocks. For perspective, Vanguard’s recommended stock allocation decreases from 90% for investors age 40 and younger to 30% for investors age 72 and older, but for all investors, it recommends that 40% of the stock allocation be invested in international stocks. Fidelity Freedom 2010 Fund (FFFCX) is intended for people who turned 65 in about 2010. Its asset allocation contains 42.06% stocks, including 55% of this stock allocation in international stocks. The T Rowe Price Retirement 2010 Fund (TRRAX) is intended for people who turned 65 in about 2010. Its asset allocation contains 43.71% stocks, including 34% of this stock allocation in international stocks. From my experience, most US investors have much lower international stock allocations than recommended by these three families of mutual funds.

In short, now would be a good time to consider your allocations to US stocks and the international portion of your total stock allocation.“

David M. Smith

Ph.D., CFA, CMA – Professor of Finance and Director, Center for Institutional Investment Management – University at Albany (SUNY), School of Business

“Businesses and consumers should be ready for higher levels of inflation than we are used to. Industry sectors that can pass along price increases quickly will be winners (e.g., consumer staples, healthcare, materials), and those that cannot be losers (e.g., consumer discretionary, air transport, some utilities). In an environment of increasing inflation, bond yields will rise, and bond prices will fall. Investors in long-term fixed-coupon bonds will suffer especially poor returns.

After COVID is brought under control, employment in most sectors will recover, restoring the strength of lagging industries like travel. Companies that cut their dividends due to COVID economic pressures will likely resume them, which should be a positive for those stock prices. At the same time, rising interest rates will drive up government borrowing costs significantly, limiting the economic stimulus that usually comes from infrastructure, education, military, and social spending.

My best advice is quite conventional.

- Stay broadly diversified across asset classes (e.g., various types of common stocks and bonds), industry sectors, and international markets.

- Weight the asset classes strategically, given your age, investment horizon, risk tolerance, and other personal characteristics.

- To gain exposure to your chosen asset classes, use low-cost index mutual funds (or ETFs) whenever possible, to take advantage of the one thing under your control – the ability to invest in vehicles that have low expense ratios.

- When stock and bond prices change and the portfolio weights deviate from your strategy weights, buy and sell the appropriate funds to bring the portfolio back into balance.

If it is irresistible to buy an individual stock you think will become a highflyer or to greatly overweight a particular industry sector, take those actions using the money you can afford to lose. Unless you have more insight into the future than most investors, you do not have a competitive edge, which makes those actions closer to gambling.

Sectors poised for future sales and earnings growth continue to be: Technology, healthcare, and transportation. However, those sectors will each have extreme winners as well as companies that fail. Also, high future growth may already be reflected in current market prices. Keep in mind the importance of buying low and selling high.”

Elven Riley

B.S. – Instructor, Department of Finance – Seton Hall University

“If you are new to investing, then please model your personal casino behavior. I am a two-pocket blackjack fan. I can play with whatever is in the left pocket, max. I buy dinner and gas for the ride home with what is in the right pocket. And the two have never been crossed. The typical rotation at this point would be out of tech and into manufacturing. I like the idea that it is time for America to start building things again and this administration is leaning into enabling that.”